The Governance Survey is conducted annually and is also used with individual clubs when we are preparing for board orientations, supplemented by the gathering of numerous supporting documents from the General Manager. Wherever possible, we also compare the survey responses with factual data to identify disconnects within the board and between board and management. The following are examples of actual misalignments and misunderstandings revealed through our analysis.

EXAMPLE 1: According to this club’s audited financial statements, it had recently entered into a multi-decade loan agreement for several million dollars with a limited prepayment penalty and a challenging debt service coverage covenant. Of the responding board members, half were seemingly unaware of the new loan. This type of response pattern is not uncommon. It highlights the need for annual board education to make sure knowledge and perceptions are accurate and consistent.

EXAMPLE 2: A club president indicated he could not pass along a 7% dues increase. He feared membership would revolt since there had “never been an increase of that magni- tude.” When told there had been an increase of more than 8% the previous year, he insisted that was not the case. We showed him the previous president’s dues announcement letter, which presented the dues increase in dollars versus a percentage, as well as the controller’s spreadsheet showing all dues by category over the last several years. The calculated year-over-year increase in the previous year had been more than 8%. Armed with that insight, the leadership team had the confidence to budget for what the club needed rather than being scared off by what they imagined would be a point of resistance.

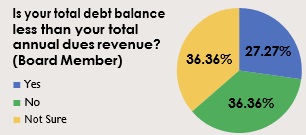

EXAMPLE 3: In this example, two-thirds of responding board members believed the club’s total debt balance was less than total annual dues revenue. In reality, the ratio at the time of our analysis was 175%. The debt-to-dues ratio is a measure of the club’s reliance on debt. Clubs with a ratio of debt to dues revenue higher than 100% are considered highly leveraged.

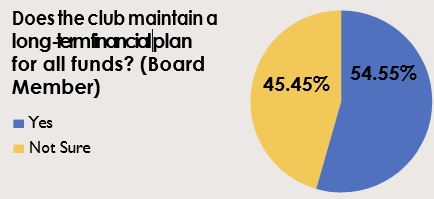

EXAMPLE 4: In this example, more than half (54%) of board members responded that the club had a long-term financial plan. The balance of respondents were not sure, which is a problem. In reality, the club did not have a long-term financial plan. Private clubs are capital intensive businesses and need to have long-term financial plans that are consistent with the strategic plan, the capital reserve study and the debt service requirements.

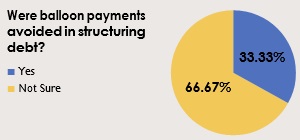

EXAMPLE 5: In this example, a third of the responding board members indicated their club did not have any balloon payments, and the others were not sure. Financial data from this club showed they did, in fact, have significant debt with a balloon payment equal to 72% of the original amount borrowed coming due in a few years.

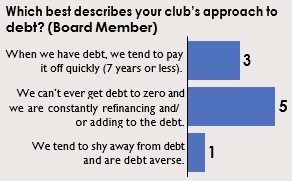

While the use of debt with balloon payments may reduce the required annual payment, it results in progressively increased borrowing costs and extends the period when the club’s available capital is encumbered and borrowing capacity is diminished. The longer repayment period also subjects the club to refinancing risks such as rate increases, less favorable terms or even the inability to refinance at all. As we like to say, boards must anticipate the capital needs future administrations will face and do their best to limit encumbrances and position those boards for success.

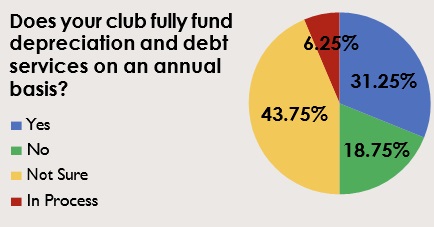

EXAMPLE 6: In this example, less than 20% of responding board members were aware that the club was not fully funding annual deprecia- tion and debt service. Financial analysis confirmed that the club was not doing so currently and had not done so for many years.

Because debt service takes priority over any other obligation, if a club is not generating sufficient capital income to fully fund depreciation and debt service, the alternative will likely be to defer obligatory capital spending. This results in the campus looking dated and tired, which will affect both current member satisfaction and new member recruitment.

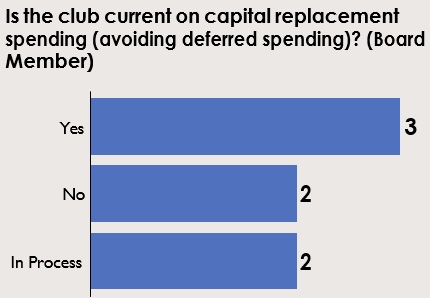

EXAMPLE 7: Of the seven responding board members, three believed the club was current on capital replacement spending. In fact, the club was not current and its net property, plant and equipment benchmark had been declining for years.